Should I Rent or Buy a House? I Did The Math and It Shocked Me.

Outdated investing advice nearly cost me half a million dollars in savings.

I’ve previously written about how our parents unwittingly pass down outdated advice on career choices and investing to their children.

Today I want to tackle an investing myth very close to home (heh).

I’m Asian. We all grew up with the idea that buying a home is not only a rite of adulthood, but also one of the best investments you can make.

The aspirational value of home ownership has been passed down for generations. It represents reaching some pinnacle in life, that you “made it”, settled down, and have a place of your own.

Renting is often seen as the temporary, inferior alternative when you cannot afford to buy.

This is particularly true in many Asian cultures, where owning property is not only a financial goal but also a symbol of prestige and security.

The problem with this idea is that it was true for so long, that nobody even bothers to check the math to see if it still remains true today.

But times have changed.

The Housing Boom Problem

One reason home ownership is such a persistent myth around the world has to do with development economics.

Generally speaking, as economies go from poor to rich, double-digit growth rates in GDP lead to rising real estate prices. Generations of people who bought homes or real estate in the early years made their fortunes from the accompanying capital gains.

The problem is that development economics also tells us double-digit GPP growth rates never last. And that directly impacts the growth in real estate prices.

However, other asset classes like equities behave very differently - because they accrue value in much more scalable ways. The S&P500 has grown 10% p.a. over the last 30 years - because it allows you to share in the astronomical growth of the world’s largest businesses, in a way that housing cannot.

Yet, these expired ideas around how people made their money, continue to stay beyond their welcome in an ever-changing world.

Should you rent, or should you buy?

To answer this question, I built a financial model using AI, and the answers really shocked me.

Let’s dive into it.

My Red Pill Moment

I have considered buying property at numerous points in my life. The closest I came to it was last year in 2023, when I was confronted with a whopping 33% rental price increase for my unit at the Icon.

Throughout my first 5 years of living in Singapore, I was lucky enough to have secured a $3K SGD monthly rental in a prime location.

But my luck had run out.

I was also making a lot less as a startup founder than as a Google employee. So I could either lose 30%+ of my salary each month, or just buy a unit at Icon.

When I floated the idea to people around me, I was cheered on by so much positive affirmation by other people that it was the right thing to do.

People would tell me things like: “Housing gets you leverage, you get to use money that isn’t yours”.

Or they would argue (quite convincingly) that renting is just wasting the money that you could have put towards building equity in an appreciating asset.

But the answer isn’t as straightforward as it seems. One of the huge missing pieces I discovered, is the invisible opportunity cost of investing your (very sizeable) downpayment.

Over a multi-decade period, that alone could return your rental expenses, plus whatever capital gains you could have made on the appreciation of your home!

I struggled to understand it at first, but stay with me.

Rent vs. Buy Calculation

I’ve made a free, publicly available calculator that anyone can use to calculate their own rent or buy decisions.

I ran the math for my own situation, and here are the numbers I used.

Buying a 1 bedroom in Icon

Home Price: $1,150,000

Stay Duration: 30 years

Mortgage Rate: 4%

Down Payment: 25% (assumed 100% comes from my pocket and not from CPF)

Length of Mortgage: 30 years

Annual upkeep costs: 2% of home value (including maintenance & repairs, tax, insurance, & other miscellaneous costs)

4.5% cost of buying the house (agent) and 8% cost of selling the home

4% projected home price appreciation

Renting a similar 1 bedroom in Icon

Monthly Rent: $4,300 (I was able to negotiate down to $4K actually but $4.3K is what is listed so I will be as objectively verifiable as possible with this and increase the amount)

Average rental growth rate of 3% annually

Other factors

I assumed investment returns in S&P 500 to be 9% (historically has been higher at nearly 11% in the last 30 years but lowered it to be conservative).

This is used to calculate the “opportunity cost” of putting money into the down payment of a house, and the other recurring expenses that apply to both buying and renting scenarios.

It turns out that I can expect to save between $1.75 million over 30 years by renting instead of buying.

A lot of this comes from (i) the opportunity cost of putting down a ~$300K downpayment instead of investing in the market, and (ii) the difference between mortgage payments and rental in many cases is minimal, especially in periods of high interest rates like the one we are currently in.

The difference between my projected mortgage payments and rental at Icon was less than $200 (other units were going for less than $100 difference in rental, but I took the higher number to be conservative).

Shocking, I know. I spent weeks re-checking the math, and running this by other people.

But I had to go with my head, and not my gut - and abandoned the plan to buy my own apartment. But I also didn’t renew my lease at Icon. I ended up down-sizing to a master bedroom in Pinnacle where I pay $2K in rent right now.

Note: Even if you re-run the calculation assuming 20% of the downpayment comes from CPF, it still makes more sense to rent instead of buy (assuming absolutely zero opportunity cost with investing CPF which I know is not true but for simplicity’s sake I just used this assumption).

This article excludes HDBs, CPF withdrawals for buying property, and the ABSD for foreigners in Singapore. If you have questions around specific calculations, I am happy to update the calculator.

What Price, Home Ownership?

That said, there are intangible benefits to owning property. For some it’s about family and stability. There is value in seeing your kids grow up in the same home and making it yours. Some really want to customize the house however they want.

Some just want the peace of mind that they won’t ever be kicked out by a landlord, or have to deal with rising rental costs with a fixed-term mortgage.

It’s just important to understand and quantify what these intangible benefits means to you. In my case, I had to ask myself if I would be willing to pay $1-2M over 30 years for these benefits.

For me, the tradeoff just wasn’t worth it. The opportunity cost was just too much for me for the intangible benefits that I personally am not prioritizing for at this time of my life.

By not buying a house and sinking a big portion of my net worth into a down payment, I am saving more deployable capital to invest in high-growth areas like AI and crypto at this stage of wealth accumulation.

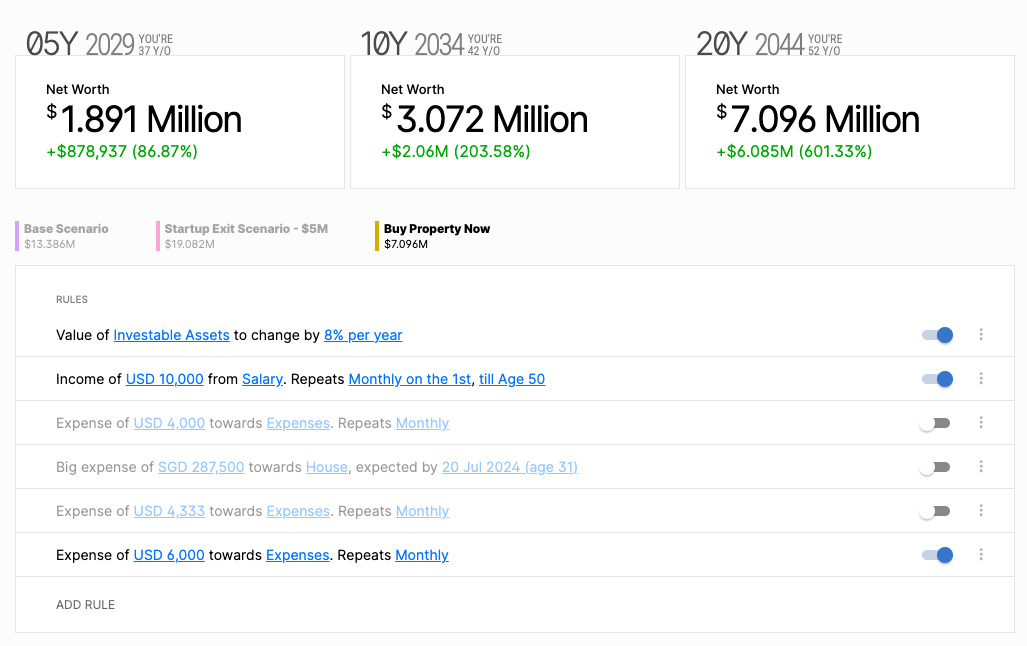

For me, getting an extra $1-2M over 30 years means being able to potentially achieve financial freedom earlier in life. Even in 10 years at age 42, there will be a close to a $900K gap in outcomes.

With an assumed inflation of 3% of costs, I won’t really be able to get financial freedom at that age, and need to get closer to my 50s for that to happen. And that’s not factoring in additional costs that may come from family planning etc.

If I look at the scenario when I don’t buy property and continue renting, then I am much closer to hitting a FIRE number of $3M around my mid-40s.

Without buying property

With buying property

The Future of Real Estate

As the world we grew up in continues to change dramatically from the one our parents made their money in, we need to update our mental models of the world.

Here are a few other things to keep in mind:

Job stability⬇️: Our parents worked at a single job with a large corporation for decades. New technologies like AI are creating more disruptions to employment, and assuming a stable income can turn out badly. Trying to support a fixed mortgage when you are laid off from your cushy job can be incredibly stressful. Our parents could easily match their fixed salary to a fixed mortgage - we might not be able to do so.

Opportunity costs ⬆️: capital markets can continue to provide higher returns because they accrue value in more scalable ways that housing cannot.

Population growth⬇️: The global population is aging and slowing. That’s not good for housing prices. Baby boomers also benefited from a booming demand for houses. We may not be able to say the same.

The problem with our mental models of the world is that our “information diet” is contaminated.

I’ve already talked about how it is contaminated by expired advice that may no longer be relevant to our generation.

But it is also contaminated by advice from people who have the wrong incentives in place. Property agents will always tell you to buy because they earn far more commissions from a sale, than from rental.

The motto for the Enlightenment during the 17th and the 18th centuries was the Latin phrase: “Sapere Aude!”: Have the courage to think for yourself.

I hope that what we’re building at Peek can make it easier for you to see, analyze, and reason from the facts in with the help of AI.

1. You mentioned that your rent went up 33%. And then assume 3% rental inflation for 30 years.

2. House you need to buy at the dip. And then assume interest rates don’t go up a lot.

3. Assumption S&P goes up linearly. Each recession it crashes 60% from peak. Unlike Covid in previous cycles takes 2-3 years to recover.

4. Housing is emotional decision.

Time to buy isnt when rent is higher but you think stability is needed.

In Istanbul where I am leaving now the percentage for mortgage is 20% per year. Inflation has been up 283% for three years (economic crisis in turkey due to dictatorship president owned decisions in economy ) and rent price has doubled in last two years.( immigrants because of war in Ukraine which russia started)