Reviewing my finances using my own AI app

Public companies review their finances in public every quarter. Since I invest in these companies, why not do the same for myself?

Reviewing my personal finances and investment portfolio helps me assess my financial health, track my progress, and make informed decisions about rebalancing my investments.

Studies done by Morningstar and Vanguard have shown that by regularly assessing your portfolio's performance, identifying areas for improvement, and making informed rebalancing decisions, you can potentially increase your returns by 1-2%.

For me, that could translate to $10-20K additional returns, which can equal to 300+ hours or 40 days worked assuming a $100K salary.

In this blog post, I'll share my insights and strategies from this quarter's review.

Eliminating Spreadsheets

Reviewing my personal finances is like sticking to a diet, or workout routine. You know it’s good for you, but it’s astonishingly difficult to develop those habits.

One reason it’s so difficult is that the activity always starts with the mind-numbing task of updating spreadsheets.

That’s why I used Peek for this review; an AI-powered app I’m working on to help you track, manage and grow your net worth.

Because my portfolio is updated in real-time, I can spend less time on manual data entry, and more time analyzing my finances with the help of dashboards and AI widgets.

I could conduct a review and put together a plan 3-4x faster than before, without having to copy-paste numbers from different bank accounts, brokerages, and crypto-wallets into an Excel spreadsheet.

The entire review and rebalancing plan was created in under 1 hour (it used to take an entire morning of 3-4 hours for me to do).

How Did My Portfolio Do?

My total net worth has grown by approximately 8% in the last three months, reaching between $1.1M to $1.2M.

This is on track with the overall target I have of 10% annualized returns each year for me to hit my long-term financial goal target in my 40s (for semi-FIRE).

Overall portfolio from Peek

Portfolio broken down by asset class in Peek.

My biggest holdings include Google (33%), SPDR S&P 500 ETF Trust (SPY) (13%), Vanguard Target Retirement Fund 2055 (13%), and Vanguard S&P 500 ETF (VOO) (7%).

When evaluating individual investments, Google and ETH emerged as top performers, with gains of 14% and 8%, respectively. Google has strong Q1 earnings and revenue, announced its first-ever dividend and $70B stock buyback, and had a slew of new product reveals at Google I/O. ETH has increased off the recent ETH ETF approval by the SEC.

On the other hand, Advanced Micro Devices (AMD) was the bottom-performing investment, with a loss of 8%. I originally invested in AMD because I wanted to have a second player/competitor to the more popular Nvidia stock that I thought could have strong growth potential. It is struggling a bit amid competition with Nvidia. This is a long-term hold for me so I need to be diversified in the AI chip space, so I needn’t worry about short-term volatility.

It's worth noting that the S&P 500 remained largely flat over the last quarter, with a modest gain of just 1%. Most of the gains in the portfolio have come from more concentrated bets than broader market movement.

Rebalancing

There are two main areas that I need to rebalance for this quarter - Google stock and cash holdings.

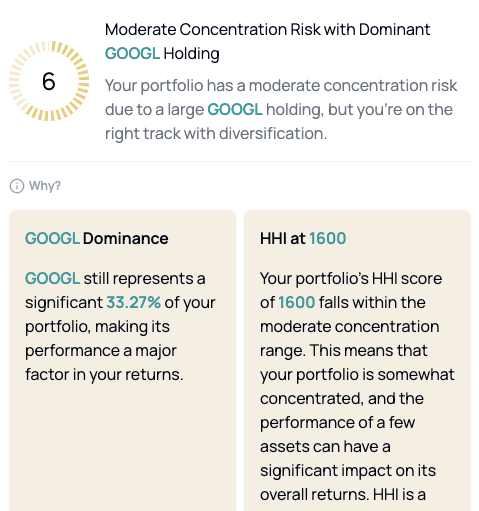

I started by running a concentration risk analysis within Peek. Peek measures concentration risk analysis through a metric called HHI Index or Herfindahl-Hirschman Index. HHI Index has also been used as a common measure of market concentration for anti-trust issues, but can also be used to determine how concentrated one individual holding can be in a portfolio.

Concentration risk analysis from Peek’s AI widget

Unsurprisingly, I have a pretty moderate concentration in Google stock, with 33% or essentially one-third of my entire portfolio in Google.

This is due partially to the fact that I used to receive a large part of my compensation in RSUs (restricted stock units) from my employment at Google and decided on a more gradual process of rebalancing rather than selling off more than $200K+ at once.

Also, Google’s share price appreciated in the last few months, which kicked up its % allocation from 31% to 33%.

Now someone might be wondering why concentration risk should be mitigated, especially since it was my concentrated bet on Google that actually increased my overall portfolio value?

Well, you don’t want to put all of your eggs in one basket because it can increase the volatility in your portfolio. Even though Google did well this quarter, during the tumultuous times in 2022 for the tech market, Google stock dropped nearly 40%.

That’s why generally most people would suggest no more than 5-10% in any given stock. I have an additional rule for myself that each 5% that I deliberately add to a stock’s weightage above 10% is if I have 10% more conviction that this company would be the dominant market leader.

With the way I’ve allocated, it would mean over 90% conviction that Google is the primary market leader in AI - as 10% + 4 * 5% = 30%.

For peace of mind, I would like to reduce my Google holdings from 33% to 20%, which still reflects strong conviction in the company, but allows my portfolio to be more diversified.

Competition from other models and the speed of execution are potential challenges to consider. However, I still believe in Google's long-term potential and maintain connections with the team to stay informed about the latest developments.

After this quarter, I will consider diversifying down even more to 15% or less, but I prefer to sell off shares gradually instead of all at once.

Peek’s AI widget also suggests some practical ways I could diversify away from Google. While the guidance is generally very high-level, it does give me food for thought about what other asset classes I could reallocate to.

Besides Google, I have some cash holdings over 3 months of expenses that I would like to invest so I don’t lose that value to inflation. All in all, I have around 15-20% of my portfolio to reallocate (from Google shares and cash) into other holders, marking one of the more significant changes I’ll make to my portfolio this year.

Rebalancing Breakdown:

To fund my rebalancing, I plan to sell some of my Google holdings, bringing my allocation down to 20%.

With the additional cash allocation, I am looking to rebalance around $180K to $220K in capital. I want the allocation for the capital to be a mix of broad market exposure, sector-specific investments, international diversification, and alternative assets.

The new allocation for these funds will be as follows (% of the $180K to $220K to deploy):

S&P 500 Index: 60%

AI Stocks: 20% (Nvidia: 8%, Microsoft: 3%, Amazon: 3%, AAPL: 3%, Palantir: 3%)

Indian ETFs: 10% (50% in Nippon India Small Cap Fund, 50% in Kotak Equity Opportunities Fund Growth)

Cryptocurrency: 10% (5% in BTC, 5% in ETH)

S&P 500 Index

This is the majority allocation because I would like most of my new funds to be relatively more stable and balanced.

AI Stocks

I always want “go where the growth is” because that is where you can find outsized returns for your portfolio.

AI is one place that’s experiencing rapid technological advancements and can contribute trillions of dollars to GDP over the next decade.

For my mix of stocks to pick for my AI bet, I actually utilized Peek’s ETF Overlap Monitor so I know my true existing mix of tech stocks. My portfolio has overlaps between direct stock holdings and indirect holdings through ETFs.

Peek’s ETF Overlap Monitor

(FYI - the small discrepancy in the ETF Overlap Monitor and the holdings % data I have above for Google is because some asset classes are excluded from the ETF Overlap Monitor including my illiquid investments in retirement funds and angel investments)

After looking at my true holdings of different AI stocks that I already have, I’ve decided on a mix of Nvidia: 8%, Microsoft: 3%, Amazon: 3%, AAPL: 3%, Palantir: 3%. None of these holdings will amount to more than 5% individually.

I’ve decided to add more to Nvidia since Nvidia is a much smaller % of my S&P 500 ETFs compared to Microsoft, Amazon, and Apple, and I do want to hold Nvidia as a second chip manufacturer alongside AMD.

Palantir is a bit of a new bet that I’m taking that is much more of a newcomer to the space - put a small 3% allocation of the amount and will monitor the stock.

Investing in India

I've decided to allocate 10% of my portfolio to Indian ETFs, as India has been one of the fastest-growing major economies in recent years.

The Nippon India Small Cap Fund has shown an impressive 20-22% annualized growth rate over the past decade, while the Kotak Equity Opportunities Fund Growth has delivered 14-16% over the same period.

Investing around $20,000 in these funds over 10 years could potentially yield returns of approximately $100,000, equivalent to a year's worth of expenses during my later FIRE years.

Just in the past year, both of these had impressive returns - 94% for Kotak and 52% for Nippon. Note that there are additional risk exposures like currency and market risk.

Cryptocurrency Allocation

I am still a long-term believer in the crypto space, even though it might take a few cycles to reach mass adoption in a meaningful way.

I'm maintaining my cryptocurrency allocation at 10%, with half in BTC and half in ETH. The expected reduction in interest rates and the approval of Bitcoin and ETH ETFs signal increased institutional adoption in the market.

As a guideline, I aim to keep my total crypto allocation under 20% and any single asset allocation to 10%.

New allocation after the changes

My new allocation would bring my ETF holdings closer to 50% of my portfolio, with Google at 20%. Crypto is now closer to 17% but still below my 20% max allocation.

Life Changes and Future Outlook:

As for significant life changes, I don't anticipate any major events or purchases in the next 3-5 years.

I'll continue to maintain a cash cushion of about $20,000, covering three months of liquidity for emergency needs.

Although the concentration risk widget suggested considering bonds or fixed income, I don't currently need to access the money and rely on my stable primary job income.

I'll revisit this strategy if any life changes require me to save up for a specific goal or need more consistent passive income.

Conclusion:

My quarterly personal finance review process might feel like extra work, but it gives me peace of mind that I am setting myself up well for my financial well-being.

1-2 hours a quarter spent on personal finance is time well-spent in my books. And this approach is not about day-trading or “timing the market” but having basic personal finance discipline to make sure that my money, and not just my time in my job, is working optimally for me.

I’m always looking to improve my quarterly review process to make it both more fun, and also more useful.

If you have any suggestions on how you approach reviewing your personal finances, feel free to reach out to me!

A lot easier to rebalance when you live somewhere without capital gains tax!

I wasn’t familiar with using HHI to score concentration risk.