Barbell: The Controversial Strategy I’m Using to Achieve Financial Independence

It's an uncommon approach to FIRE, here's why

Like many people, I want to be able to achieve financial independence/retire early (“FIRE”), but I’m taking a different strategy to getting there.

Conventional FIRE wisdom tells you to save aggressively, sometimes even up to 70% of your income, to achieve FIRE. But that means giving up a lot of the lifestyle I want to have during the healthier years of my life - where I have energy to travel, socialize and have fun.

Also, conventional FIRE says to be conservative and balanced in your investments, typically aiming to achieve a 5-7% rate of return assuming a balanced portfolio of stocks and bonds.

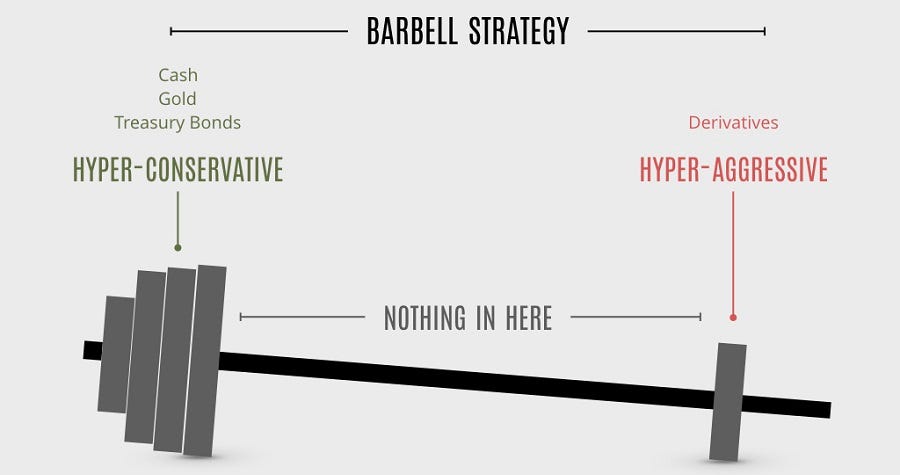

There is a new strategy to achieving FIRE that I want to talk about called the Barbell strategy. The Barbell strategy takes on more risk, to accomplish your financial goals earlier in life.

It is a somewhat controversial strategy within the FIRE community. But let me explain why it could be interesting for those who prefer to achieve financial independence earlier, without living like a scrooge.

What is a Barbell Strategy?

The barbell strategy was outlined by Taleb in his book The Black Swan: The Impact of the Highly Improbable.

A typical “balanced” portfolio of stocks or funds covering different market segments or geographic areas, tends to be spread so thin that they offer limited upside in good times, and large downside in market crashes.

In contrast, Taleb’s approach invests at the extremes in the hopes of offering more protection on the downside - with more potential upside as well.

This is achieved by constructing your portfolio in terms of both stable assets (ETFs, bonds, etc.) and growth assets (e.g., individual tech stocks, crypto, angel investing).

In the best case top 10-20% scenarios, you might be able to reap outsized benefits of that portfolio and reach your FIRE goal sooner.

But in the bottom 10% of the scenarios, you still are doing okay because you still have stable assets that ground your portfolio.

Stable Core Investments: The bulk of your investments are placed in stable, low-risk assets like index funds, bonds, or other fixed-income securities. These investments ensure steady growth and provide a safety net.

High-Risk Ventures: A smaller, yet significant, portion of your portfolio is dedicated to high-risk, high-reward investments. These could be in areas like individual stocks, cryptocurrencies, startups, or other speculative assets. The potential high returns from these investments can accelerate your path to financial independence.

The Controversy

Barbell FIRE strategy is not without its detractors. One of the biggest criticisms is investing into incredibly high-risk investments which are often speculative and have a high rate of failure.

To borrow a metaphor from poker, traditional FIRE followers often compare their investment approach to playing poker conservatively, sticking to the safest and most reliable hands. They would be playing premium hands like AA, KK, QQ, AK. More often than not, you would be winning the hand, often with a good pair.

Whereas Barbell FIRE you would be playing those exact hands but also hands like 87 suited, while riskier, can potentially deliver outsized returns by making a straight or a flush.

The best and most profitable poker players are actually the ones with a “balanced range” of both the premium hands, and the higher-risk hands as well.

Similarly, proponents of the Barbell FIRE strategy emphasize the importance of carefully combining high-risk investments with stable, conservative options. By constructing their portfolio as such, they can mitigate overall risk while maintaining the potential for significant returns.

How I’m Using the Barbell Strategy (Actual Numbers)

In a previous article, I actually talked about how I made my first million in my early 30s, and it wasn’t just through investing in index funds.

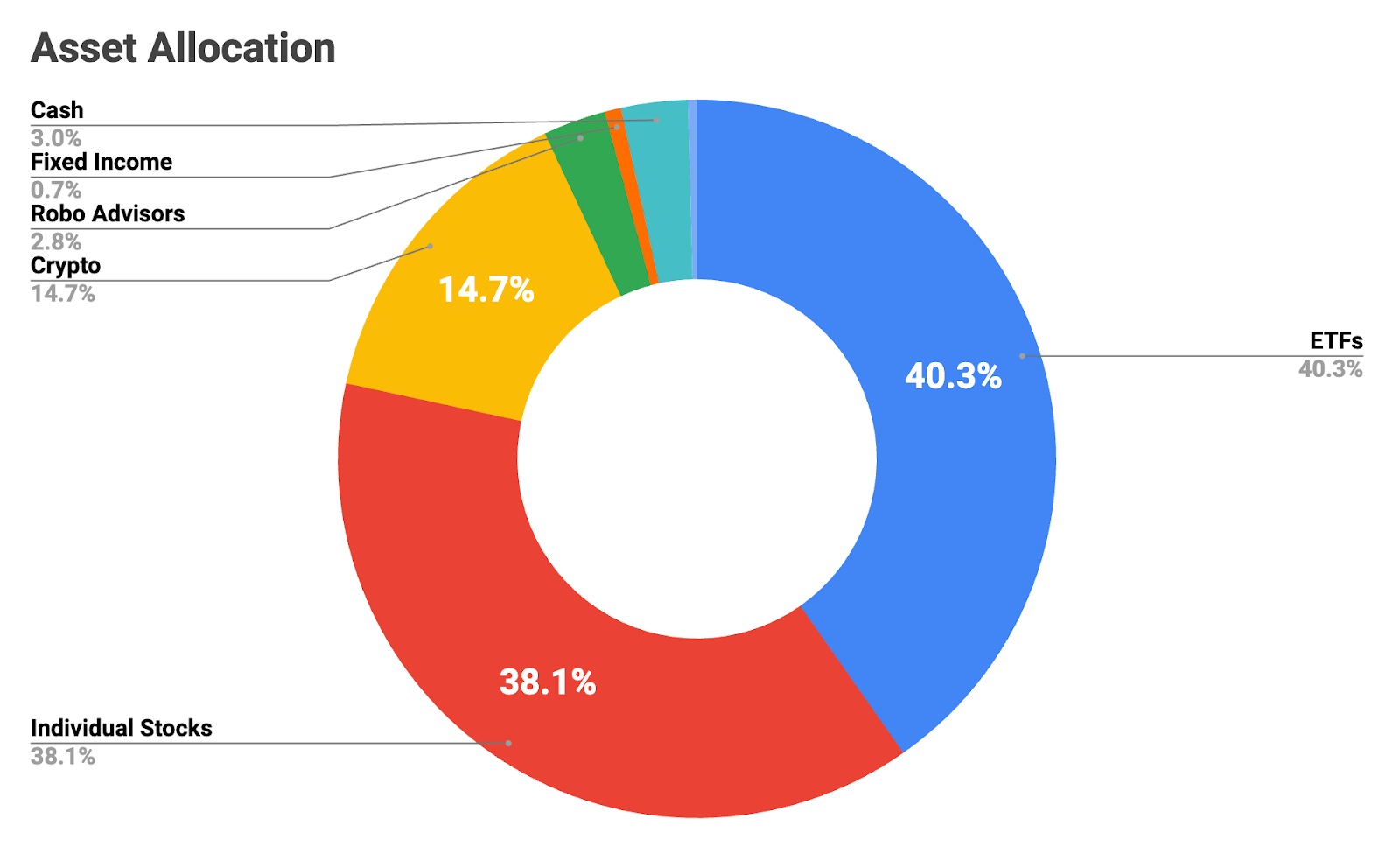

While nearly half my net worth is been invested into ETFs (between $500-$600K) - the rest of my portfolio is in higher risk assets like individual stocks (Google, Tesla, AMD) and crypto.

A big part of the reason I was able to get to my net worth in my 30s is the risk I took earlier in my life with my investing into more volatile, but high growth sectors like crypto, tech, and AI, where I think there are outsized returns for bets that you could take.

I’m aiming to achieve financial independence around my 40s and 50s.

To help me do the math, I built a FIRE calculator to see where I would be around 45. You can also use it to see if this strategy could work for you.

There are many other FIRE calculators out there, but what makes this one a bit different is it gives you:

a) More granular options for specific asset classes

b) Simulates of potential outcomes (using Monte Carlo method)

c) Better lens for the "Barbell FIRE" method

Note: For the Monte Carlo simulation, this is assuming a normal distribution for simplicity. There are of course assets that follow more of a structure with fat tails. Monte Carlo simulation is also running 1K simulations using the variables provided. Remember, simulations are just simulations and should not be treated as definitive predictors of the future.

In this first scenario, I used the assumptions much closer aligned to my current portfolio construction:

~$1.1M of current savings

50% stable vs. 50% growth assets

Stable asset return: 7% w/ 10% standard deviation

Growth asset return: 15% w/ 40% standard deviation

Annual savings to be invested: $30K

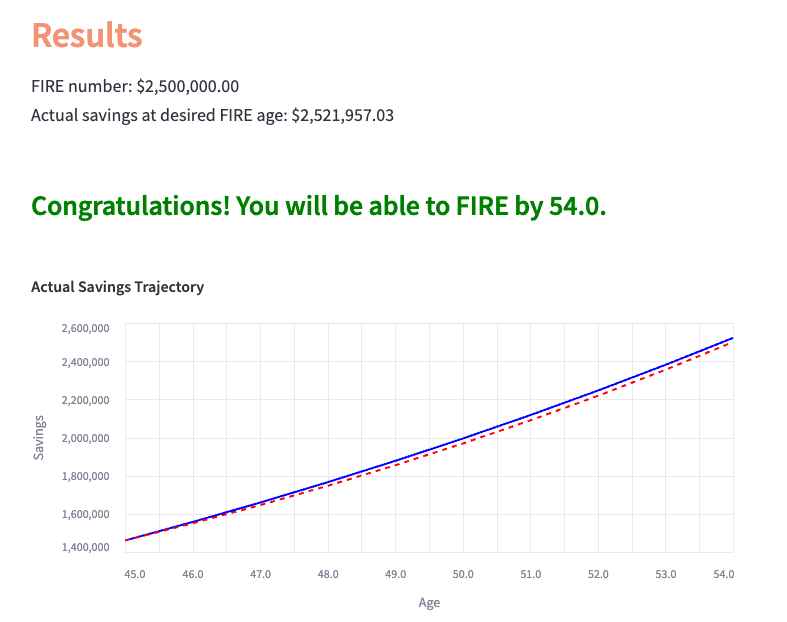

$100K annual spend per year to reach $2.5M FIRE number

What you see in the results is that I have a range of outcomes.

My best-case scenario being $6.7M at the 90th percentile (crypto goes to the moon, my AI-related investments all do well), and my worst-case at the 10th percentile being $1.3M (technology sector goes through a winter, AI-thesis does not play out, crypto is dead).

Because I still have 50% of my portfolio in stable assets, I still actually manage to grow my portfolio, albeit to the point where it just addresses inflation (~2-3%).

And there’s a whole middle range of outcomes where I would reach $2.5M by 45 to hit my FIRE goal, with the 50th percentile number being $3.1M.

What happens if I don’t adopt the Barbell strategy? Using the calculator, I tweaked the numbers so that the stable assets are 100% of the portfolio, with all else being equal.

With a maximally-conservative portfolio, you’ll notice a much narrower range of outcomes in the simulation, with the worst case being $1.5M and the best case scenario being $3.2M.

However, I will miss my FIRE goal of $2.5M by nearly $400K.

Interestingly enough, my worst-case scenario at the 10th percentile with a portfolio of 100% stable assets, is only $100K higher than the 10th percentile scenario with a portfolio of 50% stable & 50% growth assets.

If I were to aim to achieve FIRE by 45, I would need to take on some risk in my portfolio to potentially get there. However, if I lose out on some level of the investment, it’s not life-changing money and I could just work a few more years for cash like I would’ve had to anyway following the more stable strategy.

In general, taking a higher risk, higher-reward approach means there’s a world where you would be able to FIRE earlier, but it could come at the cost of having to work a few more years if you end up in the worst-case outcome.

In my model, if all of my investments outside of stable go to zero, I could still manage to FIRE at 54 which I would be more than happy with since I’m relatively flexible.

Managing Risk with Barbell FIRE

Remember: higher risk doesn’t mean you just YOLO, with zero risk management.

Allocating an appropriate portion of their portfolio to high-risk assets based on their individual risk tolerance and financial circumstances. For some, it might be 20%, for others it might 50%+

Diversifying their high-risk investments across different asset classes and sectors to minimize the impact of any single investment's failure. Instead of putting all of eggs in the crypto basket, spread it across venture investing, tech stocks, and small-to-medium businesses.

Regularly monitoring and rebalancing portfolio to maintain desired risk exposure.

Knowing when to cut losses around high-risk investments

Who Barbell FIRE Is For (Or Not)?

People who have higher risk appetite. The high-risk investments included in Barbell FIRE, such as cryptocurrencies, tech startups, or speculative stocks, can be extremely volatile. This volatility can lead to significant losses, which might not be suitable for all investors, especially those with lower risk tolerance.

People who enjoy learning about high-growth industries, and don’t mind spending time trying to find some alpha in the market.

People who are self-sufficient investors: you need to be accountable to your outcomes. Barbell FIRE requires a careful balance between low-risk and high-risk investments. This balancing act can be complex and time-consuming, necessitating a higher level of financial literacy and active portfolio management compared to more straightforward FIRE strategies.

People who have more years ahead to work in case the strategy does not work out. If you are closer to the typical retirement age, you might not want to risk it and might want to default to a more fixed-income-heavy, conservative strategy. Barbell FIRE is better for people where financial independence is a good option, but not a necessity at a certain age

People who do not have a lot of liquidity needs and dependents. Right now, I manage my own money and do not have multiple dependents where risk-taking could be an issue.

I am clearly fine with risk - I quit my corporate job to pursue a startup a few years back.

I currently do not have any dependents, where my liquidity needs are tied up.

Conclusion

There are many pathways to FIRE, each with different tradeoffs that suit different types of investors.

While Barbell FIRE may not be a mainstream approach to achieving financial independence and early retirement, it offers a win-win scenario for those willing to take on more risk in pursuit of potentially higher returns.

By strategically allocating a portion of their portfolio to high-risk, high-reward assets while maintaining a safety net of stable, low-risk investments, investors can potentially fast-track their path to financial freedom without compromising their long-term financial security.

As with any investment strategy, careful planning, risk management, and discipline are essential to maximizing the potential benefits of Barbell FIRE.

For those who still want a more traditional view of FIRE can check out these resources:

Coast FIRE: https://walletburst.com/tools/coast-fire-calc/

Barista FIRE: https://walletburst.com/tools/barista-fire-calc/

FIRE calculator: https://walletburst.com/tools/fire-calculator/

Fat FIRE: https://walletburst.com/tools/fat-fire-calculator/

And there are even niche communities within FIRE now. Andre Nader has a great FAANG Fire community: